Ramping up charging infrastructure, offering financial solutions, introducing mandates and aligning state policies with national ambition is key to accelerating e-mobility

The turn of 2020 has been an inflection point for e-mobility in India. The sector has been showing early signs of success with overall sales growing year on year and even reaching three figure growth. Going forward as well, several sales forecasts from industry and think tanks point to a promising future for electric vehicles in this decade. This is also significant from the perspective of India’s journey towards achieving net zero emissions by 2070.

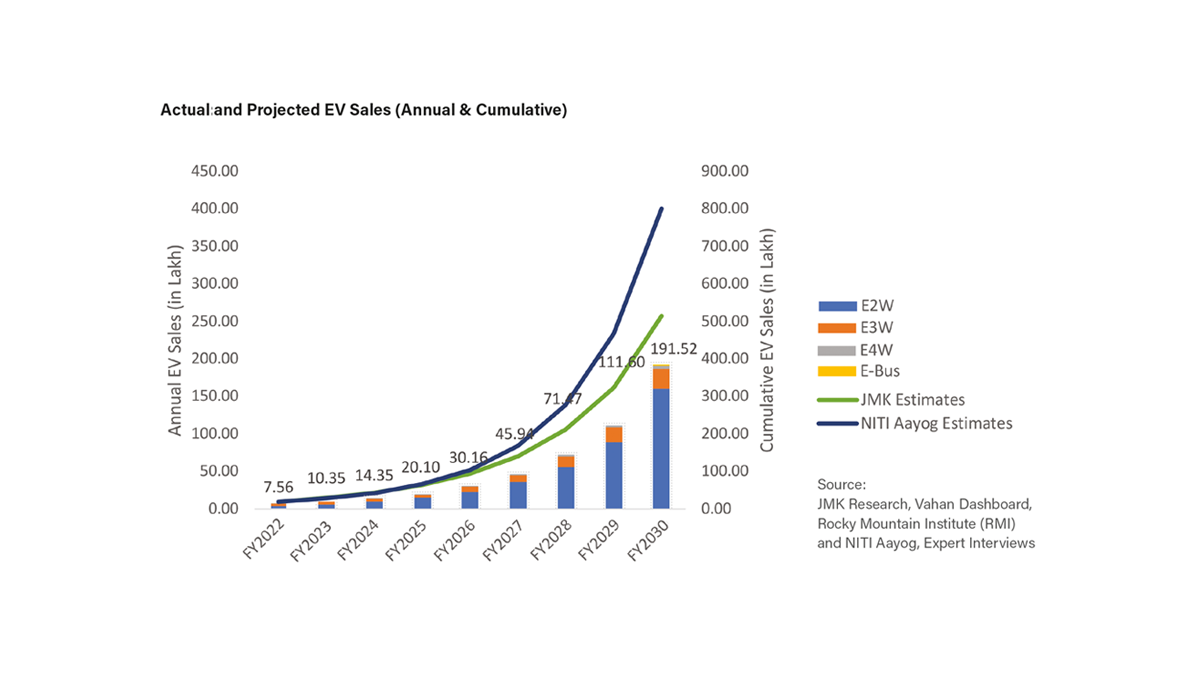

However, despite recognition of the need to decarbonize the transport sector, India does not have a national target for transport electrification. When FAME I was launched, it aimed to achieve 6 – 7 million EVs and hybrids on road by 2020. As of March 2022, we stand as 1.3 million EVs, clearly having missed the only clear target for the country. In the absence of a national target, an EV sales projection made by NITI Aayog is popularly quoted as a milestone or vision that the country can hope to achieve, in order to significantly decarbonize road transport. This projection says that if FAME II and other measures are successful, India could realize EV sales penetration of 30% of private cars, 70% of commercial cars, 40% of buses and 80% of two and three-wheelers by 2030. In absolute numbers, this amounts to having 8 crore electric vehicles on road by 2030.

While the sharp growth in EVs in the last two years has been promising, a recent report by Climate Trends and JMK Research highlights that under the current wave of electric mobility policies (FAME II, state policies), and even accounting for increased adoption in a few years as battery prices drop and local manufacturing ramps us, the country may only be able to reach 5 crore EV sales by 2030, falling behind by 40% on the sales projections by NITI Aayog. This indicates the need for more policy and industry action to accelerate EV penetration in the country.

The new analysis further estimates that India needs to have at least 39 lakh cumulative public and semi-public charging stations between 2022 and 2030, to support 8 crore EVs (based on 8 EVs per charging station). This is much higher than the charging stations planned so far in this period. It also analyses all approved state EV policies, and makes a strong case for better and more ambitious state targets to complement India’s sales projections. While some states have defined targets as absolute numbers, others have defined a percentage of total vehicles, and some have no target defined at all. Very few policies define targets for charging infrastructure or to convert government owned vehicle fleets to EVs. Moreover, the majority of the policies do not have timelines till 2030, they currently only provide support till 2022 to 2026.

Aarti Khosla, Director, Climate Trends, said, “Electric vehicles are commercially viable today. There is a very significant role of EVs in India’s road to net zero emissions. Progress on clean energy goals, for example renewable energy, happened as much due to state policies as it did due to regulation. In electric mobility as well, the country needs much more coordination. India has started on the right foot on e-mobility, with an enabling policy landscape and sales growing rapidly in some vehicle segments. However, we need more coordinated efforts between states and centre, in defining targets and incentives that align with national ambition and policies, not to miss much greater focus on charging infrastructure and financial solutions for funding EVs.”

When asked what immediate steps could help improve India’s chances of meeting the 8 crore sales forecast, Jyoti Gulia, Founder & CEO, JMK Research said, “To bridge the 40% gap in realising projected sales by 2030, India can put simple yet effective practices in place. All states must define clear targets for ramping up charging infrastructure, incentives alone are not enough. This is a prerequisite that will define adoption trends in the country. Following global examples, India should consider introducing mandates for 100% electrification of government fleets, and mandating at least some percentage of vehicle aggregator fleets to be electric.”

The study outlines a set of 6 recommendations that can improve India’s chances of realising EV sales projections by 2030. These focus on coordinated efforts across state policies and relevant government departments, and better alignment with national targets; focusing on 100% electrification of government owned and aggregator fleets; introducing mandates for EVs, especially for government vehicles and three wheelers in select cities; offering financial solutions to OEMs, battery manufacturers and consumers; and defining clear targets in state policies for charging infrastructure.

With their implementation, India stands a good chance of converting its ICE vehicles to EVs. Given the prevalence of small vehicles such as 2Ws, 3Ws, economy 4Ws and small goods vehicles in the country, India has an opportunity to take a leadership role in the electrification of small vehicles. Add to this, huge oil import bills which the country is estimated to save every year, with the conversion of over 3.99 crore two-wheelers in India to EVs. What is needed is for the industry and central and state governments to bring in key resources, technology, financing, and incentives together to create a self-sustaining EV ecosystem.